years of refreshing the world

The Coca‑Cola Company has been refreshing the world and making a difference for over 138 years. Explore our Purpose & Vision, History and more.

We've established a portfolio of drinks that are best positioned to grow in an ever-changing marketplace.

From trademark Coca‑Cola to Sports, Juice & Dairy Drinks, Alcohol Ready-to-Drink Beverages and more, discover some of our most popular brands in North America and from around the world.

Our purpose is to refresh the world and make a difference. See how our company and system employees make this possible every day and learn more about our areas of focus in sustainability.

We aim to improve people's lives, from our employees to those who touch our business to the many communities we call home.

We believe working at The Coca‑Cola Company is an opportunity to build a meaningful career while helping us make a real difference on a global scale.

Catch up on the latest Coca‑Cola news from around the globe - from exciting brand innovation to the latest sustainability projects.

Global Unit Case Volume Grew 2% for the Quarter and 2% for the Full Year

Net Revenues Grew 7% for the Quarter and 6% for the Full Year;

Organic Revenues (Non-GAAP) Grew 12% for the Quarter and 12% for the Full Year

Operating Income Grew 10% for the Quarter and 4% for the Full Year;

Comparable Currency Neutral Operating Income (Non-GAAP) Grew 20% for the Quarter and 16% for the Full Year

Fourth Quarter EPS Declined 2% to $0.46; Comparable EPS (Non-GAAP) Grew 10% to $0.49;

Full Year EPS Grew 13% to $2.47; Comparable EPS (Non-GAAP) Grew 8% to $2.69

Cash Flow from Operations Was $11.6 Billion for the Full Year, Up 5%;

Full-Year Free Cash Flow (Non-GAAP) Was $9.7 Billion for the Full Year, Up 2%

Company Provides 2024 Financial Outlook

ATLANTA, Feb. 13, 2024 – The Coca‑Cola Company today reported fourth quarter and full-year 2023 results. “During the year, our people and partners rose to meet new challenges, allowing us to excel globally and deliver in a dynamic world,” said James Quincey, Chairman and CEO of The Coca‑Cola Company. “As we begin a new year, we’re confident that our all-weather strategy, powerful portfolio and harmonized system will continue to create value for our stakeholders in 2024 and for the long term.”

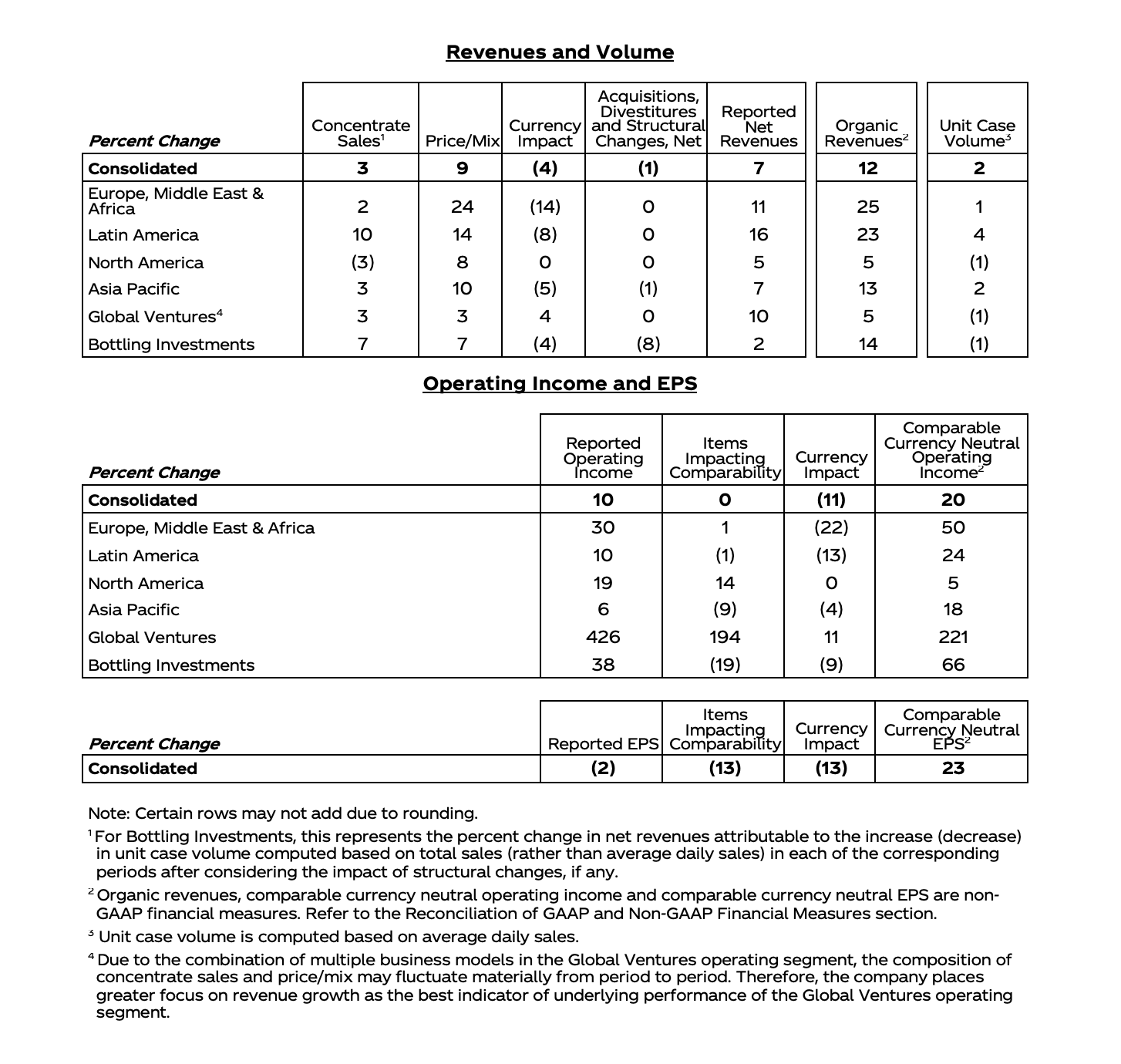

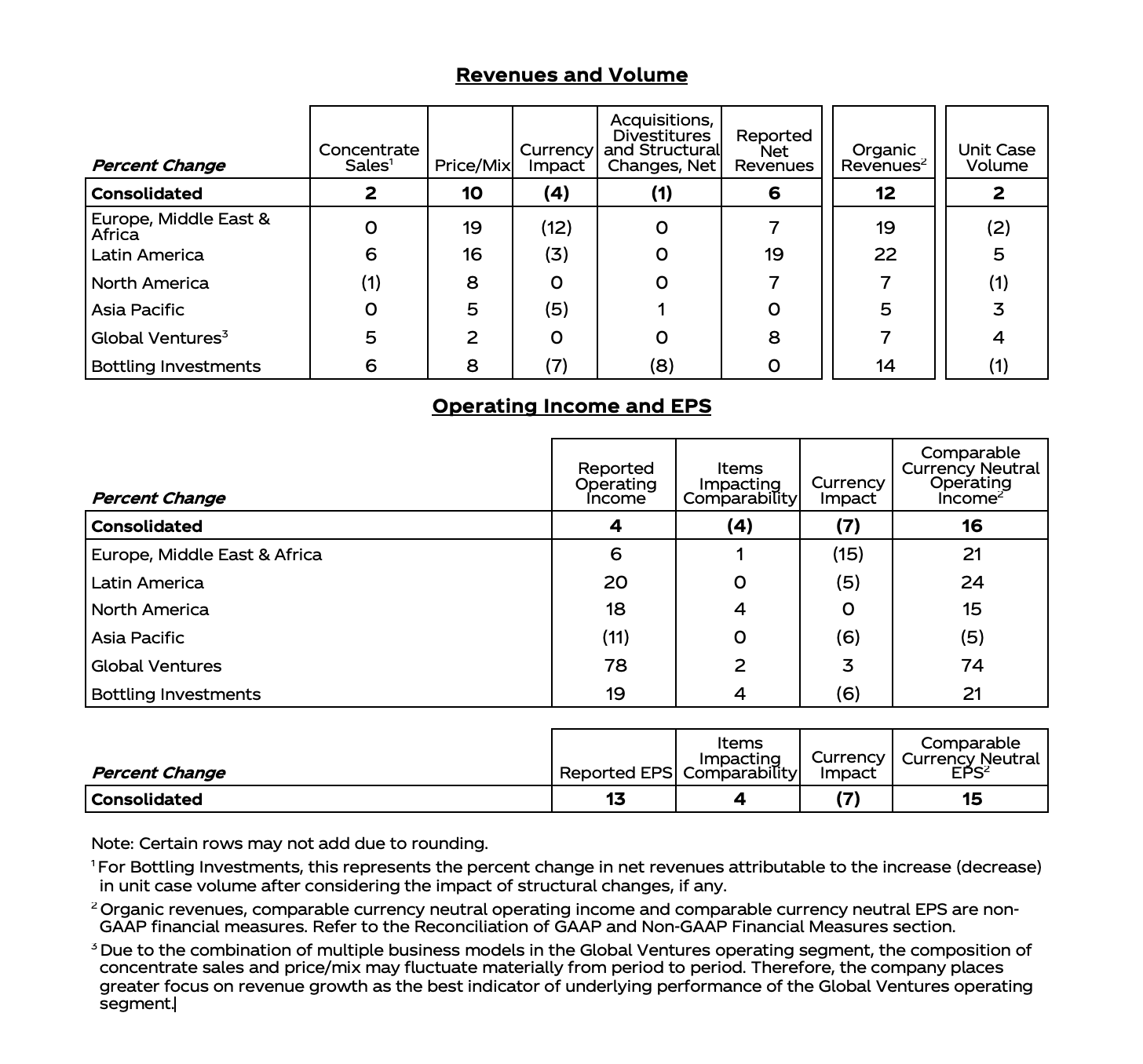

- Revenues: For the quarter, net revenues grew 7% to $10.8 billion, and organic revenues (non-GAAP) grew 12%, driven by 9% growth in price/mix and 3% growth in concentrate sales. The quarter included one additional day, which resulted in a 1-point tailwind to revenue growth. For the full year, net revenues grew 6% to $45.8 billion, and organic revenues (non-GAAP) grew 12%, driven by 10% growth in price/mix and 2% growth in concentrate sales. For both the quarter and the full year, organic revenue (non-GAAP) performance was strong across all operating segments.

- Operating margin: For the quarter, operating margin was 21.0% versus 20.5% in the prior year, while comparable operating margin (non-GAAP) was 23.1% versus 22.7% in the prior year. For the full year, operating margin was 24.7% versus 25.4% in the prior year, while comparable operating margin (non-GAAP) was 29.1% versus 28.7% in the prior year. Operating margin performance included items impacting comparability and currency headwinds. For both the quarter and full year, comparable operating margin (non-GAAP) expansion was primarily driven by strong topline growth, partially offset by an increase in marketing investments versus the prior year, as well as currency headwinds.

- Earnings per share: For the quarter, EPS declined 2% to $0.46, while comparable EPS (non-GAAP) grew 10% to $0.49. EPS performance included the impact of a 14-point currency headwind, while comparable EPS (non-GAAP) performance included the impact of a 13-point currency headwind. For the full year, EPS grew 13% to $2.47, and comparable EPS (non-GAAP) grew 8% to $2.69. EPS performance included the impact of an 8-point currency headwind, while comparable EPS (non-GAAP) performance included the impact of a 7-point currency headwind.

- Market share: For both the quarter and the full year, the company gained value share in total nonalcoholic ready-to-drink (NARTD) beverages.

- Cash flow: Cash flow from operations was $11.6 billion for the full year, an increase of $581 million versus the prior year, driven by strong business performance and working capital initiatives, partially offset by a transition tax payment and currency headwinds. Free cash flow (non-GAAP) was $9.7 billion for the full year, an increase of $213 million versus the prior year.

- Connecting with consumers through experiences and digital engagement: The company continues to leverage its marketing transformation to build globally scaled marketing platforms tailored to local consumers. In the fourth quarter, “The World Needs More Santas” campaign was executed in over 80 markets, continuing the company’s rich history of celebrating the holidays. The company leveraged the success of its first AI-based platform, “Create Real Magic”, by inviting consumers to create sharable, digital greeting cards featuring iconic brand assets such as cherished depictions of Santa Claus and the Coca‑Cola polar bear. Local initiatives generated buzz and excitement, such as the Coca‑Cola Caravan Truck Tour, which travelled throughout nearly 60 countries around the world making over a thousand stops and meeting over 16 million consumers to share in the magic. In total, the holiday campaign experiences garnered approximately 9 billion impressions on social media. By combining the company’s global scale with local relevancy, the holiday activation contributed to Trademark Coca‑Cola® volume and value share gains as well as unit case volume and transactions growth for both the quarter and for the full year.

- Building a system that is increasingly positioned for sustainable long-term growth: Since the start of 2023, the company completed the refranchising of company-owned bottling operations in Vietnam to a subsidiary of Swire Pacific Limited (Swire), completed the sale of its stake in the bottler in Pakistan to Coca‑Cola İçecek and completed the sale of its stake in the bottler in Indonesia to Coca‑Cola Europacific Partners (CCEP). More recently, the company completed the refranchising of a portion of its company-owned bottling operations in India to existing franchise bottlers and received regulatory approval to sell its bottling operations in the Philippines to CCEP and Aboitiz Equity Ventures, which is expected to close towards the end of February 2024. Additionally, the company recently completed the sale of its stake in the largest bottler in Thailand to Swire and existing shareholders of the bottler. Our franchise business model has enabled the company to develop a strong global footprint with a local touch in markets around the world. The company continuously works to optimize the system with trusted, capable and motivated bottling partners allowing it to focus on building and growing consumer-loved brands.

- Delivering on our purpose by empowering people to drive growth: The company’s strategy is centered around people, starting with the employees who are critical in bringing this strategy to life. In November, the company was ranked #1 on the 2023 American Opportunity Index, which assessed how effectively companies enable employees to progress in their careers in the United States. Around the world, the company provides thousands of jobs and is invested in the long-term success of its employees. Over the year, the company enhanced its learning and related technologies, making strides towards nurturing a more innovative and informed workforce. The company’s 2023 Culture & Engagement Survey results underscore the strong levels of employee pride and growth opportunities with a strong number of respondents saying they are proud to work at The Coca‑Cola Company and see good opportunities to learn and grow in their roles.

In addition to the data in the preceding tables, operating results included the following:

- Unit case volume grew 2% for the quarter. Developed markets were even as growth in Mexico and Germany was offset by declines in the United States and Chile. Developing and emerging markets grew 4%, driven by growth in Brazil and India. For the full year, unit case volume grew 2%. Developed markets grew 1%, driven by growth in Mexico and Germany. Developing and emerging markets grew 2%, driven by growth in India and Brazil, partially offset by the suspension of business in Russia in 2022.

Unit case volume performance included the following:

- Sparkling soft drinks grew 2% for both the quarter and the full year, primarily driven by growth in Latin America and Asia Pacific. Trademark Coca‑Cola® grew 2% for both the quarter and the full year, primarily driven by growth in Latin America and Asia Pacific. Coca‑Cola Zero Sugar grew 4% for the quarter and 5% for the full year, driven by growth in Latin America and North America. Sparkling flavors grew 1% for both the quarter and the full year, primarily driven by growth in Asia Pacific.

- Juice, value-added dairy and plant-based beverages grew 6% for the quarter and 2% for the full year. This performance benefited from growth in Minute Maid® Pulpy in China, Mazoe® in Africa and fairlife® in the United States.

- Water, sports, coffee and tea was even for the quarter and grew 1% for the full year. Water grew 1% for the quarter and 2% for the full year, primarily driven by growth in Latin America. Sports drinks declined 1% for the quarter and were even for the year. Full year performance was benefited by growth in Powerade® in Latin America, offset by a decline in BODYARMOR®. Coffee declined 7% for the quarter and grew 3% for the year. Full year performance was benefited by strong performance of Costa® coffee in the United Kingdom and China. Tea was even for the quarter and declined 1% for the full year, as growth in Latin America and Europe, Middle East and Africa was more than offset by declines in North America and doğadan® in Türkiye.

- Price/mix grew 9% for the quarter and 10% for the full year, primarily driven by pricing actions in the marketplace, including the continued impact of hyperinflationary markets, and favorable mix. For the quarter, concentrate sales were 1 point ahead of unit case volume, primarily due to one additional day.

- Operating income grew 10% for the quarter and 4% for the full year, which included items impacting comparability and currency headwinds. Comparable currency neutral operating income (non-GAAP) grew 20% for the quarter and 16% for the year. For both the quarter and the full year, performance was driven by organic revenue (non-GAAP) growth across all operating segments, partially offset by an increase in marketing investments.

- Unit case volume grew 1% for the quarter, driven by growth in water, sports, coffee and tea as well as juice, value-added dairy and plant-based beverages. Growth was led by Germany and Nigeria.

- Price/mix grew 24% for the quarter, approximately one-third of which was driven by the continued impact of pricing in hyperinflationary markets and the remaining driven primarily by pricing actions across operating units. For the quarter, concentrate sales were 1 point ahead of unit case volume, primarily due to one additional day.

- Operating income grew 30% for the quarter, which included a 22-point currency headwind. Comparable currency neutral operating income (non-GAAP) grew 50% for the quarter, primarily driven by organic revenue (non-GAAP) growth across all operating units.

- For the year, the company gained value share in total NARTD beverages, led by share gains in Türkiye, Nigeria and Germany.

- Unit case volume grew 4% for the quarter, driven by growth in Trademark Coca‑Cola and water, sports, coffee and tea. Growth was led by Brazil and Mexico.

- Price/mix grew 14% for the quarter, primarily driven by the continued impact of inflationary pricing in Argentina and pricing actions, partially offset by incremental investments in the marketplace. For the quarter, concentrate sales were 6 points ahead of unit case volume, primarily due to one additional day and the timing of concentrate shipments.

- Operating income grew 10% for the quarter, which included a 15-point currency headwind and items impacting comparability. Comparable currency neutral operating income (non-GAAP) grew 24% for the quarter, primarily driven by strong organic revenue (non-GAAP) growth, partially offset by an increase in marketing investments.

- For the year, the company gained value share in total NARTD beverages, led by share gains in Brazil, Colombia and Mexico.

- Unit case volume declined 1% for the quarter, as growth in juice, value-added dairy and plant-based beverages and Trademark Coca‑Cola was more than offset by a decline in water, sports, coffee and tea.

- Price/mix grew 8% for the quarter, primarily driven by pricing actions already in the marketplace, timing related adjustments and favorable category mix. For the quarter, concentrate sales were 2 points behind unit case volume, primarily due to the timing of concentrate shipments, partially offset by one additional day.

- Operating income grew 19% for the quarter, which included items impacting comparability. Comparable currency neutral operating income (non-GAAP) grew 5% for the quarter, primarily driven by organic revenue (non-GAAP) growth.

- For the year, the company gained value share in total NARTD beverages, driven by sparkling soft drinks and value-added dairy beverages.

- Unit case volume grew 2% for the quarter, primarily driven by growth in juice, value-added dairy and plant-based beverages and sparkling flavors. Growth was led by India and China.

- Price/mix grew 10% for the quarter, primarily driven by pricing actions in the marketplace and favorable category mix. For the quarter, concentrate sales were 1 point ahead of unit case volume, primarily due to one additional day.

- Operating income grew 6% for the quarter, which included items impacting comparability and a 13-point currency headwind. Comparable currency neutral operating income (non-GAAP) grew 18% for the quarter, driven by organic revenue (non-GAAP) growth across all operating units and lower operating costs, partially offset by an increase in marketing investments.

- For the year, the company gained value share in total NARTD beverages, led by share gains in India, the Philippines, South Korea and Japan.

- Net revenues grew 10%, and organic revenues (non-GAAP) grew 5% for the quarter, primarily driven by the strong performance of Costa® coffee in the United Kingdom and China.

- Operating income and comparable currency neutral operating income (non-GAAP) both had robust growth for the quarter, driven by organic revenue (non-GAAP) growth and lower costs.

- Unit case volume declined 1% for the quarter, as growth in India and the Philippines was more than offset by the impact of refranchising bottling operations.

- Price/mix grew 7% for the quarter, driven by pricing actions across most markets.

- Operating income grew 38% for the quarter, which included items impacting comparability and an 8-point currency headwind. Comparable currency neutral operating income (non-GAAP) grew 66% for the quarter, driven by organic revenue (non-GAAP) growth, partially offset by higher operating costs.

- Reinvesting in the business: The company continued to invest in its various lines of business and spent

$1.9 billion on capital expenditures in 2023, an increase of 25% versus the prior year.

- Continuing to grow the dividend: The company paid dividends totaling $8.0 billion during 2023. The company has increased its dividend in each of the last 61 years.

- M&A initiatives: In 2023, the company did not make any significant acquisitions. The company continues to evaluate inorganic growth opportunities through brands and capabilities. In 2023, with respect to divestitures, the company made progress towards refranchising company-owned bottling operations.

- Share repurchases: In 2023, the company issued $0.5 billion of shares in connection with the exercise of stock options by employees and purchased $2.3 billion of shares. Consequently, net share repurchases (non-GAAP) were $1.7 billion. The company’s remaining share repurchase authorization is approximately $6 billion.

The 2024 outlook information provided below includes forward-looking non-GAAP financial measures, which management uses in measuring performance. The company is not able to reconcile full-year 2024 projected organic revenues (non-GAAP) to full-year 2024 projected reported net revenues, full-year 2024 projected comparable net revenues (non-GAAP) to full-year 2024 projected reported net revenues, full-year 2024 projected underlying effective tax rate (non-GAAP) to full-year 2024 projected reported effective tax rate, full-year 2024 projected comparable currency neutral EPS (non-GAAP) to full-year 2024 projected reported EPS, or full-year 2024 projected comparable EPS (non-GAAP) to full-year 2024 projected reported EPS without unreasonable efforts because it is not possible to predict with a reasonable degree of certainty the exact timing and exact impact of acquisitions, divestitures and structural changes throughout 2024; the exact timing and exact amount of items impacting comparability throughout 2024; and the exact impact of fluctuations in foreign currency exchange rates throughout 2024. The unavailable information could have a significant impact on the company’s full-year 2024 reported financial results.

The company expects to deliver organic revenue (non-GAAP) growth of 6% to 7%.

For comparable net revenues (non-GAAP), the company expects a 2% to 3% currency headwind based on the current rates and including the impact of hedged positions, in addition to a 4% to 5% headwind from acquisitions, divestitures and structural changes.

The company’s underlying effective tax rate (non-GAAP) is estimated to be 19.2%. This does not include the impact of ongoing tax litigation with the IRS, if the company were not to prevail.

Given the above considerations, the company expects to deliver comparable currency neutral EPS (non-GAAP) growth of 8% to 10% and comparable EPS (non-GAAP) growth of 4% to 5%, versus $2.69 in 2023.

Comparable EPS (non-GAAP) percentage growth is expected to include a 4% to 5% currency headwind based on the current rates and including the impact of hedged positions, in addition to an approximate 2% headwind from acquisitions, divestitures and structural changes.

The company expects to generate free cash flow (non-GAAP) of approximately $9.2 billion through cash flow from operations of approximately $11.4 billion, less capital expenditures of approximately $2.2 billion. This does not include any potential payments related to ongoing tax litigation with the IRS.

Comparable net revenues (non-GAAP) are expected to include an approximate 4% currency headwind based on the current rates and including the impact of hedged positions, in addition to an approximate 2% headwind from acquisitions, divestitures and structural changes.

Comparable EPS (non-GAAP) percentage growth is expected to include an approximate 8% currency headwind based on the current rates and including the impact of hedged positions, in addition to an approximate 1% headwind from acquisitions, divestitures and structural changes.

The first quarter has one less day compared to the first quarter of 2023.

- All references to growth rate percentages and share compare the results of the period to those of the prior year comparable period, unless otherwise noted.

- All references to volume and volume percentage changes indicate unit case volume, unless otherwise noted. All volume percentage changes are computed based on average daily sales in the fourth quarter, unless otherwise noted, and are computed on a reported basis for the full year. “Unit case” means a unit of measurement equal to 192 U.S. fluid ounces of finished beverage (24 eight-ounce servings), with the exception of unit case equivalents for Costa non-ready-to-drink beverage products which are primarily measured in number of transactions. “Unit case volume” means the number of unit cases (or unit case equivalents) of company beverages directly or indirectly sold by the company and its bottling partners to customers or consumers.

- “Concentrate sales” represents the amount of concentrates, syrups, beverage bases, source waters and powders/minerals (in all instances expressed in unit case equivalents) sold by, or used in finished beverages sold by, the company to its bottling partners or other customers. For Costa non-ready-to-drink beverage products, “concentrate sales” represents the amount of beverages, primarily measured in number of transactions (in all instances expressed in unit case equivalents) sold by the company to customers or consumers. In the reconciliation of reported net revenues, “concentrate sales” represents the percent change in net revenues attributable to the increase (decrease) in concentrate sales volume for the geographic operating segments and the Global Ventures operating segment after considering the impact of structural changes, if any. For the Bottling Investments operating segment for the fourth quarter, this represents the percent change in net revenues attributable to the increase (decrease) in unit case volume computed based on total sales (rather than average daily sales) in each of the corresponding periods after considering the impact of structural changes, if any. For the Bottling Investments operating segment for the full year, this represents the percent change in net revenues attributable to the increase (decrease) in unit case volume after considering the impact of structural changes, if any. The Bottling Investments operating segment reflects unit case volume growth for consolidated bottlers only.

- “Price/mix” represents the change in net operating revenues caused by factors such as price changes, the mix of products and packages sold, and the mix of channels and geographic territories where the sales occurred.

- First quarter 2023 financial results were impacted by one less day as compared to first quarter 2022, and fourth quarter 2023 financial results were impacted by one additional day as compared to fourth quarter 2022. Unit case volume results for the quarters are not impacted by the variances in days due to the average daily sales computation referenced above.

The company is hosting a conference call with investors and analysts to discuss fourth quarter and full-year 2023 operating results today, Feb. 13, 2024, at 8:30 a.m. ET. The company invites participants to listen to a live webcast of the conference call on the company’s website, http://www.coca-colacompany.com, in the “Investors” section. An audio replay in downloadable digital format and a transcript of the call will be available on the website within 24 hours following the call. Further, the “Investors” section of the website includes certain supplemental information and a reconciliation of non-GAAP financial measures to the company’s results as reported under GAAP, which may be used during the call when discussing financial results.

This press release may contain statements, estimates or projections that constitute “forward-looking statements” as defined under U.S. federal securities laws. Generally, the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “will” and similar expressions identify forward-looking statements, which generally are not historical in nature. Forward-looking statements are subject to certain risks and uncertainties that could cause The Coca‑Cola Company’s actual results to differ materially from its historical experience and our present expectations or projections. These risks include, but are not limited to, unfavorable economic and geopolitical conditions, including the direct or indirect negative impacts of the conflict between Russia and Ukraine and conflicts in the Middle East; increased competition; an inability to be successful in our innovation activities; changes in the retail landscape or the loss of key retail or foodservice customers; an inability to expand our business in emerging and developing markets; an inability to successfully manage the potential negative consequences of our productivity initiatives; an inability to attract or retain a highly skilled and diverse workforce; disruption of our supply chain, including increased commodity, raw material, packaging, energy, transportation and other input costs; an inability to successfully integrate and manage our acquired businesses, brands or bottling operations or an inability to realize a significant portion of the anticipated benefits of our joint ventures or strategic relationships; failure by our third-party service providers and business partners to satisfactorily fulfill their commitments and responsibilities; an inability to renew collective bargaining agreements on satisfactory terms, or we or our bottling partners experience strikes, work stoppages, labor shortages or labor unrest; obesity and other health-related concerns; evolving consumer product and shopping preferences; product safety and quality concerns; perceived negative health consequences of certain ingredients, such as non-nutritive sweeteners and biotechnology-derived substances, and of other substances present in our beverage products or packaging materials; failure to digitalize the Coca‑Cola system; damage to our brand image, corporate reputation and social license to operate from negative publicity, whether or not warranted, concerning product safety or quality, workplace and human rights, obesity or other issues; an inability to successfully manage new product launches; an inability to maintain good relationships with our bottling partners; deterioration in our bottling partners’ financial condition; an inability to successfully manage our refranchising activities; increases in income tax rates, changes in income tax laws or the unfavorable resolution of tax matters, including the outcome of our ongoing tax dispute or any related disputes with the U.S. Internal Revenue Service (“IRS”); the possibility that the assumptions used to calculate our estimated aggregate incremental tax and interest liability related to the potential unfavorable outcome of the ongoing tax dispute with the IRS could significantly change; increased or new indirect taxes; changes in laws and regulations relating to beverage containers and packaging; significant additional labeling or warning requirements or limitations on the marketing or sale of our products; litigation or legal proceedings; conducting business in markets with high-risk legal compliance environments; failure to adequately protect, or disputes relating to, trademarks, formulas and other intellectual property rights; changes in, or failure to comply with, the laws and regulations applicable to our products or our business operations; fluctuations in foreign currency exchange rates; interest rate increases; an inability to achieve our overall long-term growth objectives; default by or failure of one or more of our counterparty financial institutions; impairment charges; an inability to protect our information systems against service interruption, misappropriation of data or cybersecurity incidents; failure to comply with privacy and data protection laws; evolving sustainability regulatory requirements and expectations; increasing concerns about the environmental impact of plastic bottles and other packaging materials; water scarcity and poor quality; increased demand for food products, decreased agricultural productivity and increased regulation of ingredient sourcing due diligence; climate change and legal or regulatory responses thereto; adverse weather conditions; and other risks discussed in our filings with the Securities and Exchange Commission (“SEC”), including our Annual Report on Form 10-K for the year ended December 31, 2022, and our subsequently filed Quarterly Reports on Form 10-Q, which filings are available from the SEC. You should not place undue reliance on forward-looking statements, which speak only as of the date they are made. We undertake no obligation to publicly update or revise any forward-looking statements.